Double Materiality

How we identify, assess and prioritise the most relevant issues for the Group

The Double Materiality Assessment is the process we used to identify the relevant sustainability issues on which to focus our actions and strategies in order to create lasting value over time and, at the same time, have a positive impact on people and the planet.

In 2025, we developed our Double Materiality Assessment following a methodological approach aligned with the requirements of Legislative Decree 2024/125, implementing Directive 2464/2022/EU (Corporate Sustainability Reporting Directive - CSRD), and the European Sustainability Reporting Standards (European Sustainability Reporting Standards - ESRS).

Scope of assessment:

The Double Materiality Assessment was carried out on all the business activities composing the Sesa Group’s Value Chain, in order to identify the impact of its activities on people and the environment (inside-out approach) and the financial relevance of ESG factors (outside-in approach), for each of the ten environmental, social and governance macro-themes identified by the new CSRD regulation.

Roles and functions involved:

The Double Materiality Assessment involved numerous departments within the Group, in particular Sustainability, Investor Relations, Accounting and Tax, Administration, Finance and Control, Human Resources and Internal Audit. The heads of each department, together with the Chief Sustainability Officer and in close collaboration with Sesa’s Chief Executive Officer, played a central role in managing the several stages of the assessment and communicating the results to the approval bodies.

The concept of ‘Double Materiality’:

Following the ESRS Standards, a sustainability issue can be considered material if it is associated with an impact, risk and/or opportunity that has emerged as relevant for one or both of the following analyses:

- Impact materiality: a sustainability issue is relevant from an impact materiality perspective if it generates impacts – actual or potential, positive or negative that are relevant to the Group, both under the direct control of the company and along its value chain, upstream and downstream. This includes the effects of its products and services and its commercial relationships on people and the environment in the short, medium and long term;

- Financial materiality: a sustainability issue is relevant from a financial materiality perspective if it generates or may generate significant financial effects for the Group, both negative (risks) and positive (opportunities). These effects have or are reasonably expected to have a significant influence on the development of the company, its financial position, economic performance, cash flows, access to financing or cost of capital in the short, medium or long term. These risks and opportunities may arise from activities carried out under the direct control of the company and along its value chain, both upstream and downstream.

Double Materiality Assessment Process Steps:

The Double Materiality process was structured into the following main phases:

- Context analysis, definition of the value chain, and identification of relevant Impacts, Risks and Opportunities (IROs): In this initial phase, the context in which the Group operates was examined, with the aim of clearly outlining the value chain. Relevant impacts, risks and opportunities related to ESG factors were then identified, considering both the Group’s own activities and upstream and downstream operations along the value chain. To carry out this phase, a top-down approach was adopted: starting from the list of sustainability matters set out in the thematic ESRS standards (as per ESRS 1, paragraph RA16), we considered the matters arising from internal processes already in place (due diligence, risk management and grievance mechanisms);

- Assessment of IROs: In this second phase, a thorough assessment of the Impacts, Risks and Opportunities identified in the previous phase was conducted. The assessment also included a further review of internal documents, relevant regulations, and validation by the functions involved in the process. Finally, to validate the results obtained, meetings were held with the Group’s top management. The top management members involved included all heads of the relevant functions, the Sustainability Committee and the Group’s Chief Executive Officer.

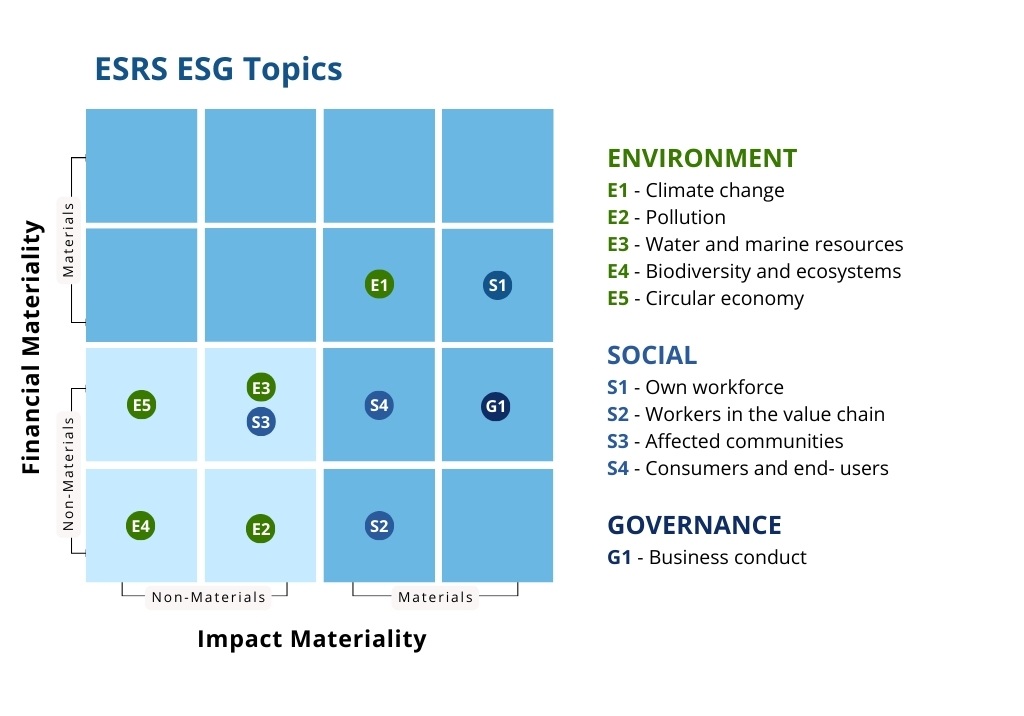

The Sesa Group's Double Materiality Matrix (FY 2025):

Developed based on the provisions of the new CSRD legislation, namely the 10 key topics defined in the European Sustainability Reporting Standards.

Based on the results of the Double Materiality Assessment, Sesa concluded that the following ESRS thematic are not relevant to the Group: pollution (ESRS E2), water and marine resources (ESRS E3), biodiversity and ecosystem protection (ESRS E4), resource use and circular economy (ESRS E5) and local communities (ESRS S3). This assessment is consistent with the nature of the Sesa Group’s activities, which operate in the IT services and technology consulting Sector, characterised by a generally limited and insignificant indirect environmental impact.

Our Sustainability Report

We follow high sustainability standards and

transparently document data, targets and results

Stakeholder Engagement

Engagement focused on inclusion, transparency, fairness,

and attention to ethical, environmental, and social issues